Why Cash Flow Problems Often Start in Accounts Receivable

A business can be profitable on paper—and still struggle to make payroll comfortably.

This is one of the most common financial challenges business owners face.

After reviewing financial statements, many owners think:

“We’re profitable. So why does cash still feel tight?”

The answer is often not sales.

It’s collections.

In recent articles, we’ve discussed bank balances, cash flow visibility, and financial reporting. Accounts receivable is where many of those issues begin to surface operationally.

A healthy receivables process helps convert completed work into collected cash.

A weak receivables process creates financial pressure long before the bank balance reflects the problem.

Executive Summary

Accounts receivable is often one of the largest assets on a business’s balance sheet.

It is also one of the most overlooked operational systems.

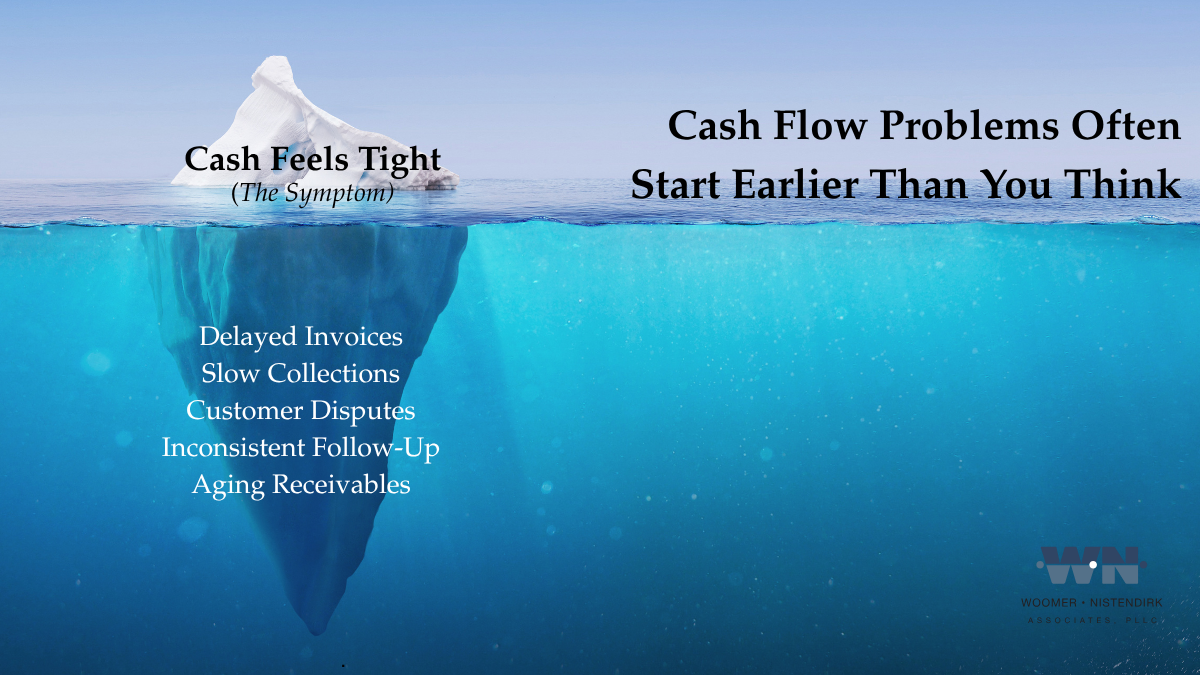

Cash flow pressure frequently stems from:

- Delayed invoicing

- Inconsistent collection procedures

- Limited visibility into aging balances

- Customer payment disputes

- Lack of accountability for follow-up

Strong receivables management improves cash flow predictability, reduces reliance on financing, and supports better decision-making.

Revenue Is Earned. Cash Is Collected.

Your income statement tells you how much revenue your business generated.

It does not tell you how much cash you actually received.

That distinction matters.

Revenue may be earned today.

Cash may not arrive for 30, 60, or even 90 days.

In other words:

Revenue is earned. Cash is collected.

The space between those two events is where many businesses experience financial pressure.

A contractor may complete a profitable month while still waiting on customer payments. A professional services firm may recognize revenue while payroll, rent, software subscriptions, and tax obligations continue to come due.

A business can be profitable and still struggle to:

- Make payroll comfortably

- Pay vendors on time

- Fund growth initiatives

- Maintain financial confidence

This disconnect is where many cash flow problems begin.

As we discussed in our cash flow visibility article, financial pressure often comes from timing gaps—not necessarily from a lack of profitability.

Where Accounts Receivable Actually Breaks Down

Collection issues rarely stem from one major mistake.

They usually develop through small breakdowns repeated consistently over time.

1. Delayed Invoicing

Work is completed.

But invoices sit waiting.

Every day an invoice remains unsent extends the collection cycle.

The longer billing is delayed, the longer cash remains unavailable.

2. Inconsistent Collection Processes

Many businesses have a billing process.

Fewer have a collection process.

Follow-up often depends on:

- Who notices the issue

- How busy the team is

- Whether the owner gets involved

This creates inconsistent results and unnecessary aging.

3. Customer Disputes

Payments frequently stall because of:

- Missing documentation

- Incorrect billing details

- Approval delays

- Service misunderstandings

Without a process to resolve disputes quickly, receivables continue to age.

4. Lack of Visibility

This is often the biggest issue.

Many businesses know their bank balance.

Fewer know:

- How much is over 30 days

- How much is over 60 days

- How much is over 90 days

- Which customers consistently pay late

Without visibility, problems remain hidden until cash becomes tight.

This is why a healthy bank balance can still be misleading. The balance tells you what is available today, but receivables help show what should be available soon. We discussed this broader visibility issue in our article on why your bank balance may not tell the full story.

Why This Becomes More Noticeable During Growth

Many owners assume growth automatically improves cash flow.

In reality, growth often amplifies receivable challenges.

Why?

Because growth usually means:

- More customers

- More invoices

- Larger balances outstanding

- More administrative complexity

As revenue increases, collection discipline becomes even more important.

A business can grow rapidly while simultaneously creating cash flow pressure if collections fail to keep pace.

Access to capital may temporarily solve liquidity issues.

But improving collections often unlocks cash that has already been earned.

As we discussed in our West Virginia funding overview, growth requires structured forecasting and disciplined financial management. Without that structure, growth can strain cash—even in a profitable business.

Accounts Receivable Pressure Often Builds Gradually

Receivable issues often develop through delayed invoicing, inconsistent follow-up, aging balances, and limited reporting visibility. Our Cash Flow & Accounts Receivable Health Checklist helps business owners identify where collection gaps may be creating cash flow pressure.

Download the Cash Flow & AR Health ChecklistWhat Strong Receivables Management Actually Looks Like

Healthy receivables systems do not depend on the owner remembering to follow up.

They are built around consistent process, visibility, and accountability.

A strong receivables system includes:

- Prompt invoicing

- Standardized payment terms

- Automated reminders

- Defined collection procedures

- Regular aging report reviews

- Clear ownership and accountability

- Consistent customer communication

The goal is not aggressive collections.

The goal is predictability.

Strong receivables management improves confidence in cash flow and allows management to make better operational decisions.

The Shift: From Reactive Collections to Intentional Cash Flow Management

Most businesses fall into a reactive receivables cycle:

- Work is completed

- Invoices are sent later than intended

- Payment terms begin after the invoice goes out

- Follow-up happens inconsistently

- Cash gets tight

- The owner steps in

A more effective approach requires consistent billing rhythms, scheduled aging reviews, defined follow-up procedures, and clear visibility into expected cash inflows.

This shift allows businesses to manage receivables proactively instead of reacting to financial pressure after it occurs.

Where This Fits Into the Bigger Picture

Over the past several months, we’ve talked about:

- Why a bank balance alone does not create financial clarity

- Cash flow forecasting and visibility

- Tax payment systems

- Funding readiness

- Financial visibility through Client Accounting Services

While those topics may appear unrelated on the surface, they are all connected by the same underlying issue:

understanding how cash moves through a business operationally.

Accounts receivable is one piece of that system.

Accounts payable, payroll, forecasting, and reporting are the next pieces.

Together, they create the visibility businesses need to operate proactively rather than reactively.

Closing Thought

Most collection problems are not caused by customers refusing to pay.

They are caused by weak processes, inconsistent visibility, and delayed action.

When businesses improve how quickly completed work becomes collected cash, they often discover that cash flow pressure eases without increasing sales.

Predictability creates confidence.

And confidence comes from visibility.

Want a Clearer Picture of Your Receivables Process?

If your business is profitable but cash still feels unpredictable, the issue may not be revenue—it may be visibility.

We’ve created a Cash Flow & Accounts Receivable Health Checklist to help business owners identify collection gaps, reporting weaknesses, and cash flow risk indicators before they create operational stress.

And if you need help building a more intentional billing, collections, and reporting structure, our team can help you create systems that support proactive decision-making—not just year-end reporting.

Request an AR & Cash Flow Review

This article is provided for general informational purposes and does not constitute legal or tax advice.