KPI Visibility: Are You Tracking Numbers or Managing Your Business?

Most business owners have access to more data than ever before.

Bank balances. Revenue reports. Payroll reports. Financial statements. Dashboard software. Industry benchmarks.

Yet many still struggle to answer simple questions:

- Are we improving?

- Are we becoming more profitable?

- Are we growing sustainably?

- What needs attention right now?

The problem is rarely a lack of data.

The problem is knowing which numbers actually matter.

Over the past several months, we’ve discussed cash flow visibility, accounts receivable, accounts payable, payroll reporting, and month-end financial reviews. Each of those areas generates valuable information.

But information alone doesn’t create better decisions.

That’s where Key Performance Indicators (KPIs) come in.

Executive Summary

KPIs help business owners focus on the small number of metrics that have the greatest influence on performance, profitability, cash flow, and growth.

The goal is not to track more numbers.

The goal is to track the right numbers consistently and use them to make better decisions.

When businesses identify the metrics that truly drive performance, they gain the ability to spot trends earlier, allocate resources more effectively, and make decisions with greater confidence.

Why Business KPI Reporting Often Fails

Many business owners assume they need more reports.

In reality, they often already have more information than they know what to do with.

Financial statements contain dozens of accounts.

Payroll reports contain hundreds of data points.

Receivables and payables reports can span multiple pages.

The challenge isn’t collecting information.

The challenge is identifying which numbers deserve management attention.

A business owner can spend hours reviewing reports and still miss the information that matters most.

Visibility is not created by more reports.

Visibility is created by knowing which numbers drive decisions.

The businesses that gain the greatest value from reporting are often not the ones with the most data.

They are the ones that consistently focus on the information most closely tied to business performance.

Not Every Number Is a KPI

One of the most common mistakes businesses make is treating every metric as equally important.

Not every number deserves a place on a dashboard.

Not every report deserves management attention.

Understanding the difference matters.

Data

Data is everything available.

Examples include individual transactions, account balances, invoices, payroll records, and operational details.

Metrics

Metrics are measurements derived from data.

Examples include revenue, payroll expense, customer counts, or average invoice size.

KPIs

KPIs are the metrics that directly influence business decisions.

They help answer questions such as:

- Are we achieving our goals?

- Are we improving or declining?

- Where should management focus attention?

- What actions need to be taken next?

A business may have hundreds of available metrics.

Only a handful are truly key performance indicators.

The goal is not to monitor everything.

The goal is to identify the numbers that matter most.

Once you’ve narrowed your focus from “everything we could measure” to “the few things we should measure,” the next step is creating a dashboard that makes those numbers part of your regular management process.

Build a KPI Dashboard That Supports Better Decisions

Knowing that not every metric deserves management attention is only the first step.

The next challenge is identifying which numbers truly drive your business—and creating a consistent process for reviewing them each month.

We’ve created a Business KPI Dashboard Planner to help you evaluate your current reporting, identify meaningful Key Performance Indicators, build a practical dashboard, and establish a monthly review process that turns reporting into better decision-making.

Download the Business KPI Dashboard Planner

Four KPI Categories Every Business Dashboard Should Include

Every business is different.

A contractor, manufacturer, medical practice, and professional services firm may track different operational metrics.

However, most businesses benefit from monitoring KPIs across four core categories.

Financial Health

These indicators help answer whether the business is generating acceptable financial results.

Examples include:

- Revenue

- Gross profit margin

- Net profit margin

- Cash position

These metrics provide a high-level view of financial performance and profitability.

Cash Flow & Liquidity

Profitability alone does not guarantee financial stability.

Cash flow indicators help measure liquidity and financial flexibility.

Examples include:

- Accounts receivable aging

- Accounts payable obligations

- Cash reserves

- Days Sales Outstanding (DSO)

These metrics help businesses understand how cash is moving through the organization.

Operational Performance

Operational KPIs help explain how efficiently the business is functioning.

Examples include:

- Payroll as a percentage of revenue

- Overtime percentage

- Capacity utilization

- Project completion rates

Operational metrics often reveal emerging issues before they appear on financial statements.

Growth Indicators

Growth metrics help determine whether expansion is occurring sustainably.

Examples include:

- New customers

- Customer retention

- Revenue per customer

- Revenue per employee

Growth is important.

Profitable growth is even more important.

The categories matter more than any specific metric.

The right KPIs are the ones that align with your business model and objectives.

Leading Indicators vs. Lagging Indicators

Not all KPIs tell the same story.

Some explain what already happened.

Others provide clues about what may happen next.

Understanding the difference can significantly improve decision-making.

Lagging Indicators

Lagging indicators measure historical performance.

Examples include:

- Revenue

- Net profit

- Gross margin

- Year-end results

These metrics are important, but they are largely backward-looking.

They tell you where you’ve been.

Leading Indicators

Leading indicators help predict future outcomes.

Examples include:

- Aging receivables

- Overtime trends

- Sales pipeline activity

- Capacity constraints

- Customer retention rates

These metrics often reveal developing issues before they affect profitability or cash flow.

Many businesses spend most of their time reviewing lagging indicators.

The strongest businesses monitor both.

Because the best KPIs help identify problems before they become financial problems.

Five Questions to Identify Your Most Important KPIs

Not every metric deserves executive attention.

To identify the KPIs that matter most, ask:

1. Does this metric influence decisions?

If the answer is no, it may not be a KPI.

2. Does this metric reveal problems early?

The best KPIs provide advance warning before issues become expensive.

3. Does this metric affect cash flow?

Cash flow remains one of the most important indicators of business health.

4. Is this metric reviewed consistently?

A KPI that is never reviewed has little value.

5. Does this metric align with our current goals?

The KPIs that matter during rapid growth may differ from those that matter during periods of stabilization or profitability improvement.

If a metric cannot help answer these questions, it may be useful information—but it may not be a true KPI.

Common Business Dashboard Mistakes

Many businesses invest significant time building dashboards.

Yet those dashboards often fail to improve decision-making.

Why?

Because the issue is rarely the dashboard itself.

Common problems include:

- Tracking too many metrics

- No clear ownership of results

- Reports that are generated but never discussed

- Metrics disconnected from business goals

- No process for taking action when trends emerge

A dashboard does not create visibility.

Consistent review and action create visibility.

The value comes from the conversation, not the software.

How CAS Turns Reporting Into Decision-Making

This is where Client Accounting Services often provide significant value.

Many businesses already have access to reports.

What they lack is structure, consistency, and interpretation.

CAS helps businesses:

- Identify meaningful KPIs

- Develop management dashboards

- Monitor trends over time

- Connect reporting to decision-making

- Improve visibility across operations

- Build accountability around performance measures

The goal is not simply to produce reports.

The goal is to create clarity.

When business owners understand which numbers matter—and what those numbers are saying—they are able to make decisions more confidently and proactively.

Where This Fits Into the Bigger Picture

Over the past several months, we’ve discussed:

- Cash flow visibility

- Why your bank balance isn’t a strategy

- Accounts receivable visibility

- Accounts payable visibility

- Payroll visibility

- Month-end visibility

- Financial visibility through Client Accounting Services

Each of those topics focused on a different piece of the financial picture.

KPIs bring those pieces together.

Accounts receivable helps explain future cash inflows.

Accounts payable helps explain future obligations.

Payroll helps explain labor costs and capacity.

Month-end reporting combines those areas into a complete financial picture.

KPIs help identify which parts of that picture deserve the most attention.

Because the goal is not to collect more data.

The goal is to create clarity.

And clarity leads to better decisions.

Closing Thought

Most businesses already have access to the information they need.

What they often lack is focus.

The strongest businesses are not necessarily tracking more numbers.

They are tracking the right numbers.

When owners consistently monitor the metrics that drive performance, profitability, cash flow, and growth, they gain the visibility needed to make better decisions and respond to challenges before they become costly.

Because success rarely comes from having more data.

It comes from understanding which numbers matter most.

Want to Identify the KPIs That Matter Most?

We’ve created a Business KPI Dashboard Planner to help business owners evaluate which metrics they’re currently monitoring, identify gaps in visibility, and determine which numbers deserve management attention.

And if you’d like help building dashboards, management reporting, or KPI review processes that support proactive decision-making, our team can help you create systems that provide clarity throughout the year—not just at year-end.

Request a KPI Visibility Review.

This article is provided for general informational purposes and does not constitute legal or tax advice.

Month-End Visibility: Are Your Financial Statements Helping You Make Decisions?

Most business owners receive financial statements.

The question is whether those statements are helping them make better decisions—or simply documenting what has already happened.

For many businesses, month-end reporting becomes a compliance exercise. The books get closed, reports get generated, and the financial statements are filed away until the next month.

But month-end reporting should do much more than document what already happened.

Done well, it becomes one of the most valuable management tools available to a business owner.

Over the past several weeks, we’ve discussed cash flow visibility, accounts receivable, accounts payable, and payroll reporting. Month-end reporting is where all of those pieces come together into a complete financial picture.

When reporting is timely, accurate, and consistently reviewed, business owners gain the visibility needed to make better decisions before problems become costly.

Executive Summary

Month-end reporting provides more than historical financial statements. It creates visibility into profitability, cash flow, operational performance, and emerging business trends.

Businesses that close their books consistently and review financial results regularly are often able to identify issues earlier and make more informed decisions.

Strong month-end visibility helps business owners:

- Understand profitability

- Monitor cash flow trends

- Identify operational issues earlier

- Evaluate staffing and labor costs

- Improve forecasting and planning

- Make decisions using data rather than assumptions

The goal is not simply to produce reports.

The goal is to create visibility.

A Common Example

Imagine it’s June 15.

Your business has money in the bank. Payroll was processed last week. Customers are still buying. On the surface, everything feels fine.

Then your month-end financial statements arrive for May.

You discover that:

- Gross margins have been declining for three months

- Overtime costs increased significantly

- Several large customer balances are now over 60 days old

- Expenses are running higher than budget

- Net profit is lower than expected despite higher sales

The challenge wasn’t necessarily business performance—it was awareness.

The issues had been developing for months, but without timely reporting they remained hidden until they began affecting profitability, cash flow, and operations.

Month-end reporting helps identify those trends while there is still time to respond.

Your Financial Statements Are a Scoreboard

Imagine coaching a football game without knowing the score until three weeks after the game ended.

That would make it difficult to adjust strategy, correct mistakes, or capitalize on opportunities.

Yet many businesses operate exactly this way.

Owners often know:

- Their current bank balance

- Whether payroll cleared

- Whether customers are paying on time

But they may not know:

- Whether the business was profitable last month

- Whether margins are improving or declining

- Whether labor costs are increasing

- Whether receivables are creating cash flow pressure

- Whether expenses are trending higher than expected

Financial statements provide the scoreboard.

Without them, owners are often forced to rely on assumptions rather than measurable performance.

The clearer the reporting, the easier it becomes to evaluate what is working—and what needs attention.

Why Delayed Reporting Creates Delayed Decisions

One of the most common issues we see is not inaccurate reporting.

It’s delayed reporting.

A business may receive perfectly accurate financial statements six or eight weeks after month-end.

The problem is that by then, the information has lost much of its value.

Imagine discovering in mid-May that profitability declined significantly in March.

The issue may already be affecting April and May operations.

The same challenge applies to:

- Increasing payroll costs

- Rising overhead expenses

- Declining margins

- Slow-paying customers

- Cash flow pressure

Financial statements should help business owners manage the future—not simply explain the past.

The longer reporting is delayed, the longer corrective action is delayed as well.

What Strong Month-End Visibility Actually Includes

Many business owners think month-end reporting means receiving a profit and loss statement.

While the income statement is important, strong reporting typically includes much more.

Individually, each report answers a different question. Together, they provide a more complete picture of business performance.

Profit & Loss Statement

The income statement helps answer:

- Are we profitable?

- Are revenues increasing?

- Are expenses growing faster than sales?

- Are margins changing?

Balance Sheet

The balance sheet helps answer:

- What do we own?

- What do we owe?

- Is our financial position strengthening or weakening?

Cash Position Review

Cash remains one of the most important resources in any business.

Reviewing cash alongside other financial information provides context that a bank balance alone cannot provide.

Accounts Receivable Review

As we discussed in our recent receivables article, revenue does not become useful until it becomes collected cash.

Aging reports help identify:

- Slow-paying customers

- Collection trends

- Potential cash flow risks

Accounts Payable Review

Payables help clarify future obligations and upcoming cash requirements.

Without visibility into accounts payable, cash flow surprises become much more likely.

Payroll Review

Payroll reporting helps owners evaluate:

- Labor costs

- Overtime trends

- Staffing requirements

- Capacity constraints

Together, these reports create the visibility needed to understand not just what happened, but why.

If you’re not sure whether your current reporting process provides this level of visibility, download our Month-End Visibility Checklist.

Download the Month-End Visibility Checklist

Most Reporting Problems Are Timing Problems

Most reporting problems are not accuracy problems.

They’re timing problems.

By the time many businesses receive their financial information, the opportunity to act on it has already passed.

Good reporting doesn’t simply explain what happened. It helps influence what happens next.

Timely reporting creates opportunities to:

- Adjust spending

- Improve collections

- Address labor issues

- Manage cash flow

- Improve profitability

Five Signs Your Month-End Process Needs Attention

While every business is different, several warning signs often indicate that month-end reporting could be improved.

1. Financial Statements Arrive More Than 30 Days After Month-End

The longer reporting takes, the harder it becomes to act on the information.

2. Cash Flow Surprises Occur Regularly

Unexpected cash pressure often indicates gaps in reporting visibility.

3. Large Adjustments Appear Every Month

Frequent corrections may suggest bookkeeping or reconciliation issues.

4. Management Decisions Depend Primarily on Bank Balances

Bank balances are important—but they are only one piece of the financial picture.

5. Reports Are Produced but Rarely Reviewed

Financial reports create value only when they support decisions.

If reports are generated but never discussed, opportunities are likely being missed.

How CAS Improves Month-End Visibility

Many business owners do not struggle because they lack financial information.

They struggle because the information arrives inconsistently, too late, or without meaningful interpretation.

This is where Client Accounting Services (CAS) can provide value.

Beyond bookkeeping and transaction processing, CAS helps businesses establish consistent reporting rhythms, improve the quality of financial data, and create structured review processes that turn reports into conversations—and conversations into decisions.

That may include:

- Consistent month-end close processes

- Financial statement preparation

- Cash flow monitoring

- Accounts receivable and payable visibility

- Payroll reporting

- Management reporting and advisory discussions

The goal is not simply cleaner books.

It is a clearer understanding of how the business is performing and where attention is needed next.

Where This Fits Into the Bigger Picture

Over the past several months, we’ve discussed:

- Cash flow visibility

- Why a bank balance isn’t a strategy

- Accounts receivable visibility

- Accounts payable visibility

- Payroll visibility

Each of these areas helps explain part of the financial story.

Month-end reporting brings those pieces together.

Receivables explain expected cash inflows.

Payables explain upcoming obligations.

Payroll explains labor costs and operational capacity.

Month-end reporting brings those individual pieces together and turns financial activity into a story that owners can understand and act upon.

And once that picture becomes clear, the next step is understanding which numbers matter most.

In our next article, we’ll explore KPI Visibility and how business owners can identify the key performance indicators that drive better decisions.

Closing Thought

Accounts receivable helps explain when cash is expected to arrive.

Accounts payable helps explain what cash is already committed.

Payroll helps explain how labor is affecting profitability.

Month-end reporting brings those pieces together into a complete picture of business performance.

When owners can clearly see what is happening inside the business, they are better equipped to respond to challenges, capitalize on opportunities, and plan for the future.

Because the goal of financial reporting isn’t simply to understand the past.

It’s to make better decisions about what comes next.

Want a More Consistent Month-End Review Process?

Many business owners receive financial statements every month. The challenge is turning those reports into meaningful conversations and better decisions.

We’ve created a Month-End Visibility Checklist to help business owners review financial performance, cash flow, receivables, payables, payroll, and emerging trends through a structured monthly process.

And if you need help creating a more consistent reporting rhythm, improving financial visibility, or building management reporting that supports proactive decision-making, our team can help you develop systems that provide clarity throughout the year—not just at year-end.

Request a Financial Visibility Review

This article is provided for general informational purposes and does not constitute legal or tax advice.

Payroll Visibility: What Your Payroll Is Trying to Tell You

Most business owners think about payroll every time employees get paid.

But payroll is more than a recurring transaction. It is often one of the largest expenses in a business and one of the clearest indicators of how operations are performing.

When payroll is viewed only as a compliance requirement, it answers a single question: Did employees get paid correctly?

When payroll is viewed as a management tool, it helps answer much bigger questions about profitability, staffing, capacity, growth, and cash flow.

Executive Summary

Payroll visibility helps business owners understand labor costs, overtime trends, staffing needs, and operational efficiency before those issues begin affecting profitability or cash flow. By monitoring key payroll metrics and reviewing labor trends regularly, owners can make better decisions about hiring, scheduling, growth, and resource allocation.

Your Payroll Is Usually Your Largest Controllable Expense

Imagine two businesses with identical revenue.

One spends 28% of revenue on payroll.

The other spends 42%.

Both may appear healthy on the surface, but they are operating very differently.

Payroll visibility helps explain why.

For many businesses, payroll represents one of the largest categories of spending each month.

Beyond employee wages, payroll costs often include:

- Payroll taxes

- Employee benefits

- Overtime pay

- Bonuses and incentives

- Paid time off

Unlike fixed expenses such as rent or insurance, payroll is dynamic. Staffing levels change. Workloads fluctuate. Overtime increases and decreases. New hires and raises affect costs throughout the year.

Because payroll is constantly changing, it deserves more attention than a quick glance at the amount withdrawn from the bank account.

Businesses that regularly monitor payroll trends often identify problems earlier and make more informed decisions about staffing and growth.

What Payroll Data Is Really Telling You

Payroll reports contain far more information than simply who was paid and how much.

When reviewed consistently, payroll data can reveal important trends throughout the business.

Most owners know what payroll cost. Fewer know what payroll is trying to tell them.

Payroll is not just an expense.

It is operational data.

Every paycheck contains information about staffing levels, workload, productivity, profitability, and future hiring needs.

Businesses that learn to read that information often identify issues sooner than those who only review payroll when cash leaves the bank account.

Overtime Trends

Overtime can provide valuable insight into operational capacity.

Consistent overtime may indicate:

- Understaffing

- Rapid business growth

- Scheduling inefficiencies

- Workload imbalances between employees

Occasional overtime is normal. Ongoing overtime may signal the need to evaluate staffing levels or operational processes.

In some cases, overtime can be less expensive than hiring additional staff. In others, it may indicate a capacity issue that deserves further review. The key is understanding which situation applies to your business.

Labor Cost Trends

A business should regularly compare payroll growth to revenue growth.

If payroll expenses are increasing significantly faster than revenue, profitability may begin to suffer even if sales remain strong.

Understanding labor cost trends helps owners make proactive decisions before margins begin to erode.

Pricing Signals

Payroll costs can sometimes reveal pricing issues before profitability concerns appear on financial statements.

If labor costs continue increasing while margins remain flat or decline, the issue may not be staffing—it may be pricing.

For example, a business may be adding employees, paying more overtime, or increasing wages while charging customers the same rates it charged two or three years ago.

Payroll visibility helps owners identify when pricing strategies need review before labor costs begin eroding profitability.

Capacity Signals

Payroll data can often reveal hiring needs before employees become overwhelmed.

Increasing overtime, reduced productivity, and rising labor costs may indicate that current staffing levels are no longer aligned with workload demands.

Businesses that monitor these signals early can often avoid burnout, turnover, and service disruptions.

Seasonal Patterns

Many businesses experience predictable fluctuations throughout the year.

Payroll reporting can help identify:

- Seasonal labor requirements

- Busy periods requiring additional staffing

- Slow periods where schedules may need adjustment

Understanding these patterns improves forecasting and budgeting throughout the year.

The challenge isn’t collecting payroll data.

Most businesses already have it.

The challenge is turning that information into decisions.

Is Your Payroll Data Working for You?

Most payroll reports show what was paid.

Few business owners take the next step and analyze what those payroll numbers are saying about labor costs, staffing needs, overtime trends, or profitability.

Our Payroll Visibility Checklist helps business owners identify labor cost trends, staffing pressures, and reporting gaps before they begin affecting profitability or cash flow.

Download the Payroll Visibility Checklist

Five Payroll Metrics Every Owner Should Monitor

While every business is different, several payroll metrics provide valuable insight across industries.

1. Total payroll cost

Track total payroll expenses over time and compare changes month-over-month and year-over-year.

2. Payroll as a percentage of revenue

This metric helps determine whether labor costs remain aligned with business performance.

3. Overtime percentage

Monitoring overtime separately can identify staffing pressures and operational inefficiencies before they become larger problems.

4. Revenue per employee

Revenue per employee can help identify whether staffing growth is keeping pace with business growth.

While no single benchmark applies to every industry, monitoring this metric over time can reveal whether additional labor investments are producing expected results.

5. Payroll trends over time

Payroll should not be viewed in isolation. Looking at trends over several months often reveals patterns that are not obvious from a single payroll cycle.

Warning Signs Hidden Inside Payroll Reports

Many business challenges appear in payroll data long before they show up elsewhere.

Common warning signs include:

- Overtime becoming routine rather than occasional

- Payroll costs increasing faster than revenue

- Frequent payroll adjustments or corrections

- Significant growth in unused PTO balances

- Repeated last-minute scheduling changes

- High employee turnover resulting in increased hiring and training costs

These issues do not necessarily indicate a problem on their own, but they deserve attention and further analysis.

Payroll Problems Often Show Up Before Financial Problems

By the time a business experiences cash flow pressure, declining profitability, or operational strain, labor-related issues may have been developing for months.

Payroll reporting often serves as an early warning system.

Reviewing payroll trends regularly can help identify concerns before they impact cash flow, customer service, or employee retention.

Businesses that proactively monitor payroll data are often able to make adjustments earlier and with fewer disruptions.

How CAS Turns Payroll Data Into Better Decisions

Processing payroll is important.

Understanding payroll is even more valuable.

Client Accounting Services can help business owners move beyond simply running payroll by providing:

- Payroll trend analysis

- Labor cost monitoring

- Overtime reporting

- Budget-to-actual comparisons

- Cash flow forecasting

- Workforce planning insights

The goal is not simply to produce payroll reports.

The goal is to help business owners answer questions such as:

- Are labor costs aligned with revenue?

- Are staffing levels sustainable?

- Is overtime supporting growth or covering a process problem?

- Are recent hiring decisions producing results?

Visibility turns payroll data into business decisions.

Where This Fits Into the Bigger Picture

Payroll visibility is another important piece of the financial visibility puzzle.

In our previous articles, we discussed how as accounts receivable visibility helps you understand when cash is expected to arrive and how accounts payable visibility helps you manage obligations and preserve cash flow.

Payroll sits directly between those two functions.

Receivables tell you when cash should arrive.

Payables tell you what cash is already committed.

Payroll tells you how effectively labor is being converted into results.

Together, receivables, payroll, and payables create a more complete picture of how cash moves through a business.

When these areas are monitored together, owners can make more informed decisions about hiring, growth, spending, and profitability.

Month-end reporting brings all three together into a complete financial picture.

In our next article, we’ll explore Month-End Visibility and why timely, accurate financial reporting is essential for turning business data into reliable decision-making.

Closing Thought

Payroll is more than a recurring transaction.

It is one of the clearest indicators of how a business is operating.

When business owners understand the story behind payroll data, they gain insight into staffing, profitability, capacity, and growth. The result is better decisions, stronger financial visibility, and greater confidence in the future of the business.

Most owners know what payroll cost.

The businesses that gain the greatest advantage are the ones that understand what payroll is trying to tell them.

Need help turning payroll data into meaningful business insights?

If payroll feels like something that simply happens every pay period, the issue may not be payroll processing—it may be visibility.

We’ve created a Payroll Visibility Checklist to help business owners identify labor cost trends, staffing pressures, overtime concerns, and reporting gaps before they begin affecting profitability or cash flow.

And if you need help building a more intentional approach to payroll reporting, labor cost monitoring, workforce planning, and financial visibility, our team can help you create systems that support proactive decision-making—not just year-end reporting.

Request a Payroll Visibility Review

This article is provided for general informational purposes and does not constitute legal or tax advice.

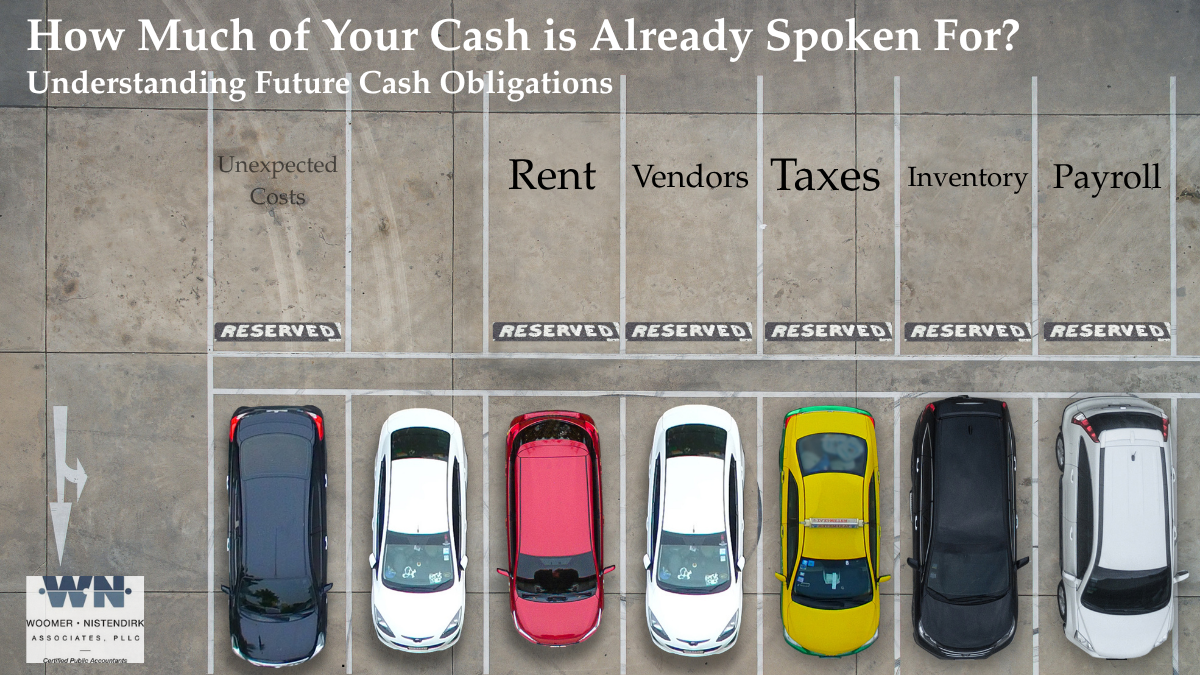

How Much of Your Cash Is Already Spoken For?

Most business owners spend a lot of time thinking about money coming into the business.

Far fewer spend time strategically managing the money going out.

After all, paying bills seems straightforward. An invoice arrives, you have the money, and you pay it.

But accounts payable is about far more than paying bills.

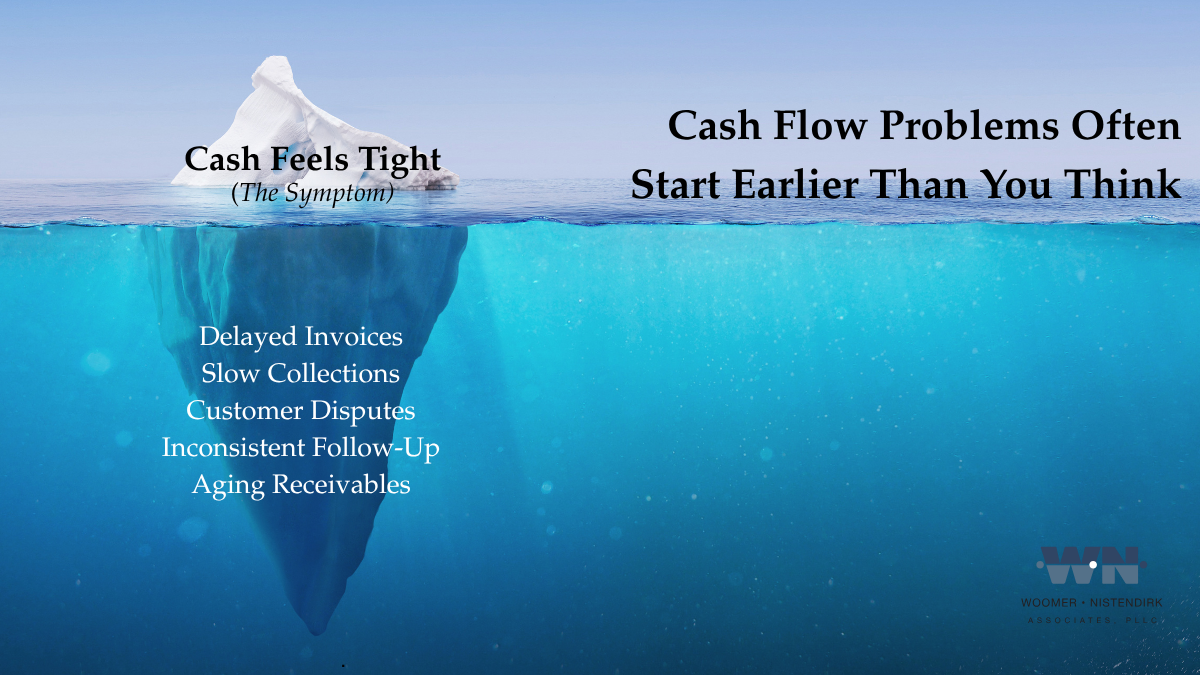

In many businesses, cash flow surprises don’t happen because owners don’t care about their finances. They happen because obligations aren’t visible until they become urgent.

Most cash flow problems are visibility problems before they become money problems.

Done well, accounts payable can improve cash flow, strengthen vendor relationships, reduce financial surprises, and provide a clearer picture of your business’s future obligations. Done poorly, it can create unnecessary cash strain even when revenue is strong.

If accounts receivable represents future cash coming into your business, accounts payable represents future cash leaving it.

Understanding both sides of that equation is essential for making informed financial decisions.

Executive Summary

Accounts payable is often viewed as an administrative function. In reality, it is one of the most important cash flow management tools available to business owners.

A well-managed accounts payable process helps businesses:

- Preserve working capital

- Improve cash flow visibility

- Avoid late fees and penalties

- Strengthen vendor relationships

- Reduce financial surprises

- Make better decisions about spending and growth

The goal is not to pay bills faster or slower.

The goal is to pay bills intentionally.

Your Bank Balance Doesn’t Tell the Whole Story

In our recent article on bank balances, we discussed why the amount showing in your checking account is only a snapshot of today’s position.

The same principle applies here.

Imagine two businesses that each have $75,000 in the bank.

At first glance, they appear equally healthy.

But one business has only $15,000 of upcoming obligations due over the next month.

The other has $120,000 of bills due within the next 30 days.

Those businesses are in very different financial positions.

Without visibility into accounts payable, a bank balance alone can create a false sense of security.

Accounts payable provides a forward-looking view of commitments that have already been made but have not yet been paid.

That information matters when evaluating hiring decisions, equipment purchases, owner distributions, or expansion plans.

The Hidden Cost of Paying Bills Too Early

Many business owners believe paying bills immediately is a sign of good financial management.

In some cases, it can actually create unnecessary pressure on cash flow.

Consider a vendor invoice with Net 30 payment terms.

If the invoice arrives on June 1 and payment is due on July 1, paying it on June 3 may not provide any additional benefit to the business.

Instead, it removes cash from your account nearly four weeks earlier than required.

That cash could have remained available for:

- Payroll needs

- Seasonal fluctuations

- Unexpected expenses

- Growth opportunities

- Emergency reserves

This does not mean businesses should delay payments beyond agreed terms.

It simply means that payment timing should be managed strategically rather than automatically.

Using available payment terms appropriately is one of the simplest ways to improve liquidity without increasing sales or borrowing additional funds.

As we discussed in our Cash Flow Visibility article, visibility into upcoming inflows and outflows often reveals opportunities to improve cash management before problems develop.

The Other Extreme: Paying Too Late

While paying too early can strain cash flow, paying too late creates a different set of problems.

Late payments can lead to:

- Vendor frustration

- Late fees and finance charges

- Credit holds

- Disrupted supply chains

- Damaged business relationships

- Reduced negotiating leverage

Many vendors view payment history as a reflection of how reliable a customer is.

Businesses that consistently pay on time often receive greater flexibility, better service, and stronger long-term relationships.

The goal is not to stretch every payment as long as possible.

The goal is to understand payment obligations and manage them intentionally.

Warning Signs Your Accounts Payable Process Needs Attention

Many cash flow issues begin long before they appear in the bank account.

Here are a few indicators that your accounts payable process may need improvement:

Bills Are Paid Based on Memory

If payment decisions rely on someone’s inbox, desk pile, or memory, important obligations can easily be overlooked.

Vendor Balances Frequently Surprise You

No business owner should be surprised by an invoice that was already received.

Unexpected bills often indicate a lack of visibility into obligations.

Multiple People Handle Bills Without Clear Processes

When invoices move through the organization without a consistent approval process, mistakes become more likely.

You Miss Early-Payment Discounts

Some vendors offer discounts for accelerated payment.

Without proper tracking, these opportunities are often missed.

Cash Shortages Seem to Appear Unexpectedly

If cash flow problems consistently feel like surprises, accounts payable visibility may be part of the issue.

How Much of Your Cash Is Already Spoken For?

A healthy bank balance can create a false sense of security if significant vendor obligations are already committed but not yet paid.

Many cash flow challenges begin weeks before they appear in the bank account. The invoices have been received. The obligations are known. What is often missing is visibility.

Our Accounts Payable Planning Worksheet helps you organize upcoming vendor payments, identify timing pressures, and gain a clearer picture of future cash needs so you can make decisions proactively rather than reactively.

Download the AP Planning Worksheet

Most Cash Flow Problems Start Before the Money Leaves the Bank

By the time a bill creates a cash crunch, the underlying issue often existed for weeks or even months.

The invoice was received.

The obligation was known.

The payment was coming.

What was missing was visibility.

The strongest accounts payable systems are not necessarily the most complex.

They simply provide clarity.

Business owners should be able to answer questions such as:

- What bills are due this week?

- What obligations are coming next month?

- Which vendors require approval before payment?

- Are any discounts available?

- How will upcoming payments affect cash flow?

When those answers are readily available, decision-making becomes easier and financial surprises become less common.

Just as accounts receivable helps businesses understand future cash inflows, accounts payable helps clarify future cash outflows. Together, they provide a more complete picture of how cash moves through the business.

Where Client Accounting Services Can Help

Many business owners don’t struggle because they can’t pay bills.

They struggle because they don’t have a complete picture of upcoming obligations until cash becomes tight.

Visibility—not transaction processing—is often the missing piece.

This is where a structured accounts payable process can create significant value.

Client Accounting Services can help businesses:

- Organize vendor invoices and payment schedules

- Improve approval workflows

- Monitor upcoming obligations

- Forecast future cash requirements

- Identify opportunities to improve payment timing

- Create better visibility into overall cash flow

The result is not simply cleaner bookkeeping.

It is better financial decision-making.

When accounts payable information is timely, organized, and accurate, owners can focus less on reacting to surprises and more on planning for growth.

Where This Fits Into the Bigger Picture

Over the past several months, we’ve talked about:

- Cash flow forecasting and visibility

- Why a bank balance alone does not create financial clarity

- Accounts receivable and collections

- Tax payment systems

- Funding readiness

- Financial visibility through Client Accounting Services

While those topics may appear unrelated on the surface, they are all connected by the same underlying issue:

understanding how cash moves through a business operationally.

Accounts payable is one piece of that system.

Accounts receivable helps explain future cash inflows.

Accounts payable helps explain future cash outflows.

Payroll, forecasting, and reporting are the next pieces.

Together, they create the visibility businesses need to operate proactively rather than reactively.

Closing Thought

Most business owners focus heavily on what customers owe them.

Fewer pay equal attention to what the business already owes others.

Yet both are critical pieces of the cash flow picture.

Accounts receivable shows future cash coming in.

Accounts payable shows future cash going out.

When you understand both, you gain a clearer view of your business’s financial reality and put yourself in a stronger position to make confident decisions.

The strongest businesses rarely eliminate every financial challenge.

What they do eliminate are surprises.

When you have visibility into both incoming and outgoing cash, you can make decisions proactively instead of reactively.

Because most financial problems are visibility problems before they become money problems.

Want a Clearer Picture of Your Accounts Payable Process?

If your business is profitable but cash still feels unpredictable, the issue may not be profitability—it may be visibility.

We’ve created an Accounts Payable Planning Worksheet to help business owners identify upcoming obligations, payment timing pressures, approval gaps, and cash flow risk indicators before they create operational stress.

And if you need help building a more intentional payment planning, approval workflows, and reporting structure, our team can help you create systems that support proactive decision-making—not just year-end reporting.

Request an Accounts Payable Review

This article is provided for general informational purposes and does not constitute legal or tax advice.

Why Cash Flow Problems Often Start in Accounts Receivable

A business can be profitable on paper—and still struggle to make payroll comfortably.

This is one of the most common financial challenges business owners face.

After reviewing financial statements, many owners think:

“We’re profitable. So why does cash still feel tight?”

The answer is often not sales.

It’s collections.

In recent articles, we’ve discussed bank balances, cash flow visibility, and financial reporting. Accounts receivable is where many of those issues begin to surface operationally.

A healthy receivables process helps convert completed work into collected cash.

A weak receivables process creates financial pressure long before the bank balance reflects the problem.

Executive Summary

Accounts receivable is often one of the largest assets on a business’s balance sheet.

It is also one of the most overlooked operational systems.

Cash flow pressure frequently stems from:

- Delayed invoicing

- Inconsistent collection procedures

- Limited visibility into aging balances

- Customer payment disputes

- Lack of accountability for follow-up

Strong receivables management improves cash flow predictability, reduces reliance on financing, and supports better decision-making.

Revenue Is Earned. Cash Is Collected.

Your income statement tells you how much revenue your business generated.

It does not tell you how much cash you actually received.

That distinction matters.

Revenue may be earned today.

Cash may not arrive for 30, 60, or even 90 days.

In other words:

Revenue is earned. Cash is collected.

The space between those two events is where many businesses experience financial pressure.

A contractor may complete a profitable month while still waiting on customer payments. A professional services firm may recognize revenue while payroll, rent, software subscriptions, and tax obligations continue to come due.

A business can be profitable and still struggle to:

- Make payroll comfortably

- Pay vendors on time

- Fund growth initiatives

- Maintain financial confidence

This disconnect is where many cash flow problems begin.

As we discussed in our cash flow visibility article, financial pressure often comes from timing gaps—not necessarily from a lack of profitability.

Where Accounts Receivable Actually Breaks Down

Collection issues rarely stem from one major mistake.

They usually develop through small breakdowns repeated consistently over time.

1. Delayed Invoicing

Work is completed.

But invoices sit waiting.

Every day an invoice remains unsent extends the collection cycle.

The longer billing is delayed, the longer cash remains unavailable.

2. Inconsistent Collection Processes

Many businesses have a billing process.

Fewer have a collection process.

Follow-up often depends on:

- Who notices the issue

- How busy the team is

- Whether the owner gets involved

This creates inconsistent results and unnecessary aging.

3. Customer Disputes

Payments frequently stall because of:

- Missing documentation

- Incorrect billing details

- Approval delays

- Service misunderstandings

Without a process to resolve disputes quickly, receivables continue to age.

4. Lack of Visibility

This is often the biggest issue.

Many businesses know their bank balance.

Fewer know:

- How much is over 30 days

- How much is over 60 days

- How much is over 90 days

- Which customers consistently pay late

Without visibility, problems remain hidden until cash becomes tight.

This is why a healthy bank balance can still be misleading. The balance tells you what is available today, but receivables help show what should be available soon. We discussed this broader visibility issue in our article on why your bank balance may not tell the full story.

Why This Becomes More Noticeable During Growth

Many owners assume growth automatically improves cash flow.

In reality, growth often amplifies receivable challenges.

Why?

Because growth usually means:

- More customers

- More invoices

- Larger balances outstanding

- More administrative complexity

As revenue increases, collection discipline becomes even more important.

A business can grow rapidly while simultaneously creating cash flow pressure if collections fail to keep pace.

Access to capital may temporarily solve liquidity issues.

But improving collections often unlocks cash that has already been earned.

As we discussed in our West Virginia funding overview, growth requires structured forecasting and disciplined financial management. Without that structure, growth can strain cash—even in a profitable business.

Accounts Receivable Pressure Often Builds Gradually

Receivable issues often develop through delayed invoicing, inconsistent follow-up, aging balances, and limited reporting visibility. Our Cash Flow & Accounts Receivable Health Checklist helps business owners identify where collection gaps may be creating cash flow pressure.

Download the Cash Flow & AR Health ChecklistWhat Strong Receivables Management Actually Looks Like

Healthy receivables systems do not depend on the owner remembering to follow up.

They are built around consistent process, visibility, and accountability.

A strong receivables system includes:

- Prompt invoicing

- Standardized payment terms

- Automated reminders

- Defined collection procedures

- Regular aging report reviews

- Clear ownership and accountability

- Consistent customer communication

The goal is not aggressive collections.

The goal is predictability.

Strong receivables management improves confidence in cash flow and allows management to make better operational decisions.

The Shift: From Reactive Collections to Intentional Cash Flow Management

Most businesses fall into a reactive receivables cycle:

- Work is completed

- Invoices are sent later than intended

- Payment terms begin after the invoice goes out

- Follow-up happens inconsistently

- Cash gets tight

- The owner steps in

A more effective approach requires consistent billing rhythms, scheduled aging reviews, defined follow-up procedures, and clear visibility into expected cash inflows.

This shift allows businesses to manage receivables proactively instead of reacting to financial pressure after it occurs.

Where This Fits Into the Bigger Picture

Over the past several months, we’ve talked about:

- Why a bank balance alone does not create financial clarity

- Cash flow forecasting and visibility

- Tax payment systems

- Funding readiness

- Financial visibility through Client Accounting Services

While those topics may appear unrelated on the surface, they are all connected by the same underlying issue:

understanding how cash moves through a business operationally.

Accounts receivable is one piece of that system.

Accounts payable, payroll, forecasting, and reporting are the next pieces.

Together, they create the visibility businesses need to operate proactively rather than reactively.

Closing Thought

Most collection problems are not caused by customers refusing to pay.

They are caused by weak processes, inconsistent visibility, and delayed action.

When businesses improve how quickly completed work becomes collected cash, they often discover that cash flow pressure eases without increasing sales.

Predictability creates confidence.

And confidence comes from visibility.

Want a Clearer Picture of Your Receivables Process?

If your business is profitable but cash still feels unpredictable, the issue may not be revenue—it may be visibility.

We’ve created a Cash Flow & Accounts Receivable Health Checklist to help business owners identify collection gaps, reporting weaknesses, and cash flow risk indicators before they create operational stress.

And if you need help building a more intentional billing, collections, and reporting structure, our team can help you create systems that support proactive decision-making—not just year-end reporting.

Request an AR & Cash Flow Review

This article is provided for general informational purposes and does not constitute legal or tax advice.

Why Your Bank Balance Isn't a Financial Strategy

You log into your business bank account and see a healthy balance. Relief sets in. Maybe there is room to hire, invest in equipment, take an owner distribution, or simply breathe a little easier.

But a bank balance only tells part of the story. What it does not show can be where the real risk lives.

For many business owners, checking the bank account becomes the default decision-making tool. It is understandable — but it can also be dangerously incomplete.

Executive Summary

Your bank balance is a snapshot, not a strategy. While cash on hand matters, it does not tell you what obligations are already committed, what timing risks are ahead, or whether your business is truly generating healthy cash flow.

In this article, we explore why bank-balance decision making can create false confidence — or unnecessary panic — and what stronger financial visibility actually looks like for business owners making operational and growth decisions.

The False Confidence of a Healthy Bank Balance

Imagine a business with $85,000 in the bank. At first glance, that may feel comfortable.

But what if payroll processes Friday, quarterly payroll taxes draft next week, insurance renewals are due, accounts payable are stacking up, and two major customer payments are late?

That same $85,000 can suddenly feel very different.

Bank balances create a moment-in-time view. Financial decisions require a forward-looking one.

What Your Bank Balance Does Not Tell You

A bank balance does not reveal the full operational picture. It does not show:

- Payroll and payroll tax obligations already approaching

- Rent, debt service, insurance, and vendor commitments

- Slow-paying receivables or customer concentration risk

- Seasonal revenue fluctuations

- Margin compression despite growing sales

- Owner draws that reduce flexibility

- Planned equipment purchases or expansion commitments

Cash visibility is not the same as cash availability.

A bank balance can show what is present today without showing what is already spoken for tomorrow.

READ MORE ABOUT CASH FLOW VISIBILITY

The Decisions Business Owners Get Wrong with Incomplete Visibility

When owners rely primarily on the bank balance, common decisions can become reactive rather than strategic.

- Hiring too early because cash looks strong

- Delaying investment because cash feels tight in a temporary cycle

- Taking owner distributions without clear forecasting

- Missing tax obligations that were not properly planned for

- Overcommitting to growth without understanding future cash pressure

None of these decisions are irrational. They simply reflect incomplete information.

What Real Financial Visibility Looks Like

Better financial decision-making starts with better questions. Instead of asking, “What is in the bank?” consider asking:

- What does the next 13 weeks of cash flow look like?

- Which receivables are outstanding, and how likely are they to collect on time?

- What obligations are already committed over the next 30 to 90 days?

- Are margins improving or shrinking?

- Where are recurring pressure points appearing?

- What decisions are coming that will require capital?

This is where financial visibility shifts from reactive monitoring to active management.

When Checking the Bank Account Becomes a Warning Sign

If your business regularly makes decisions by logging into online banking, waiting for month-end surprises, or wondering whether payroll will clear comfortably, the issue may not simply be revenue.

It may be visibility.

Many growing businesses eventually outgrow reactive bookkeeping. Historical recordkeeping remains important — but leadership decisions require insight into what is coming next, not just what already happened.

If your cash position feels unpredictable, the real question may not be “Do we have enough revenue?”

It may be: “Do we have enough visibility?”

Where Better Systems Create Better Decisions

Strong financial operations are not just about keeping the books current. They help create clarity around timing, obligations, trends, and decision readiness.

For some businesses, that means implementing stronger cash flow forecasting. For others, it means improving receivables visibility, expense discipline, or management reporting.

This is where client accounting services can support more than historical recordkeeping. The goal is not just accurate books. It is stronger business decisions.

Not Sure Where Financial Visibility Is Breaking Down?

If financial decision-making feels more reactive than intentional, stronger visibility may be the missing piece. Our Financial Clarity Checklist helps business owners evaluate the operational and reporting blind spots that often create cash stress, delayed decisions, and reactive management.

Download the Cash Flow Visibility Worksheet

This article is provided for general informational purposes and does not constitute legal, tax, or financial advice.

Why Profitable Businesses Still Run Out of Cash

A business can be profitable on paper—and still feel like it’s constantly short on cash.

This is one of the most common (and most misunderstood) financial challenges business owners face.

After tax season, many owners review their results and think:

“We made money… so why does it still feel tight?”

The answer is almost never tax-related.

It’s operational.

Over the past several months, we’ve discussed payroll tracking, tax payment systems, funding readiness, and financial visibility. Cash flow is where all of those operational decisions finally intersect.

Executive Summary

Cash flow issues are rarely caused by a lack of profitability. Instead, they stem from how money moves through your business.

In most cases, the pressure comes from:

- Timing gaps between revenue and cash collection

- Limited visibility into upcoming obligations

- Operational decisions made without cash flow forecasting

- Inconsistent systems for managing receivables, payables, and payroll

Strong business cash flow visibility allows owners to make proactive decisions before financial pressure builds.

Profit Doesn’t Equal Cash

Your income statement tells you whether your business is profitable.

It does not tell you whether you have cash available when you need it.

That’s because profit includes:

- Revenue that hasn’t been collected yet

- Expenses that haven’t been paid yet

- Non-cash items like depreciation

In other words:

Profit is a calculation.

Cash is reality.

Timing is what determines whether a profitable business actually feels financially stable day to day.

A contractor may finish a profitable month on paper while still waiting on receivables, facing payroll on Friday, equipment payments on Monday, and quarterly taxes the following week.

A business can show strong profits and still struggle to:

- Make payroll comfortably

- Pay vendors on time

- Invest in growth opportunities

This disconnect is where most financial stress begins.

Where Cash Flow Actually Breaks Down

Cash flow issues don’t come from one big mistake.

They come from small breakdowns across the financial system.

1. Revenue Timing (Accounts Receivable)

You’ve earned the revenue—but you haven’t been paid yet.

Common issues include:

- Delayed invoicing

- Inconsistent follow-up

- Long payment cycles

This creates a lag between “earning” and “having.”

2. Expense Timing (Accounts Payable)

Bills are paid based on urgency—not strategy.

This often looks like:

- Paying everything immediately “to stay safe”

- Or delaying payments without a clear plan

Both approaches create unnecessary pressure on cash.

Tax payments often create additional pressure here because businesses may know an obligation is coming but have not proactively reserved the liquidity for it, as we discussed in our IRS Direct Pay overview.

3. Payroll Pressure

Payroll is usually the largest recurring expense in a business.

And it’s fixed.

Unlike other costs, it can’t easily be delayed or adjusted in the short term.

We also see:

- Overtime creeping in without planning

- Staffing decisions made reactively instead of strategically

Payroll is often where operational inefficiencies become financially visible first.

Even recent overtime reporting changes highlighted how important accurate payroll tracking and labor visibility have become for businesses managing recurring cash obligations.

4. Lack of Forward Visibility

This is the biggest issue.

Most businesses operate based on:

- Current bank balance

- Recent activity

Instead of:

- What’s coming in over the next 4–8 weeks

- What obligations are already committed

Without forward visibility, businesses begin making decisions based on stress instead of strategy.

Why This Becomes More Noticeable After Tax Season

Tax season creates a temporary sense of clarity.

You:

- Review your financials

- File your return

- See your results

But shortly after, the reality sets back in:

The tax return is backward-looking.

Your business operates forward.

That’s why post-tax season is often the ideal time to reassess cash flow systems, forecasting, and operational planning—not just tax strategy.

Tools like IRS Direct Pay can make executing tax payments more efficient.

But execution isn’t the issue.

The issue is:

- When the cash is available

- And whether the payment fits into your broader cash flow

Growth Makes This Worse—Not Better

Many business owners expect cash flow to improve as they grow.

In reality, growth often amplifies the problem.

Why?

Because growth requires:

- Hiring before revenue is fully realized

- Purchasing inventory or equipment upfront

- Extending credit to customers

As we discussed in our West Virginia funding overview, accessing capital requires structured forecasting and disciplined financial management.

Without that structure, growth can strain cash—even in a profitable business.

Access to capital may solve a temporary liquidity issue, but without cash flow discipline, growth itself can become the source of financial strain.

Cash Flow Is Where Operational Decisions Become Financial Pressure

Every operational decision affects the movement of cash through a business.

Businesses rarely lose financial stability all at once. More often, pressure accumulates gradually through operational decisions that were never evaluated through a cash flow lens.

Pressure builds on liquidity through:

- Payroll decisions

- Tax obligations

- Vendor payment terms

- Delayed invoicing and collections

- Hiring and growth initiatives

Without strong reporting and forward visibility, these pressures often remain hidden until they begin impacting day-to-day operations.

Cash flow problems are rarely isolated accounting issues.

More often, they are operational decisions showing up financially.

Cash Flow Pressure Often Builds Gradually

Most cash flow problems develop gradually through timing gaps, payroll pressure, delayed collections, and reactive decision-making. Our Cash Flow Visibility Worksheet helps business owners map upcoming inflows, obligations, and pressure points before they begin impacting operations.

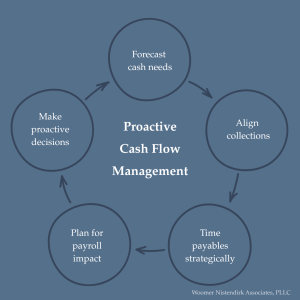

Download the Cash Flow Visibility WorksheetWhat Strong Cash Flow Actually Looks Like

Stable businesses don’t eliminate variability—they manage it proactively.

A strong cash flow system includes:

- Clear visibility into cash position weekly

- Short-term forecasting (typically 4–13 weeks)

- Planned timing of receivables and payables

- Awareness of payroll impact on liquidity

- Consistent reporting rhythms and review processes

- Decision-making based on data—not bank balance

The goal isn’t perfection.

It’s predictability.

The Shift: From Reactive to Intentional

Most businesses operate in a reactive cycle:

- Cash comes in

- Bills get paid

- Payroll hits

- Cash gets tight

- Repeat

A more effective approach requires consistent visibility, forecasting, and operational planning across the business.

This shift allows businesses to make decisions proactively instead of reacting to financial pressure after it occurs.

Where This Fits Into the Bigger Picture

Over the past several months, we’ve talked about:

- Payroll and overtime tracking

- Tax payment systems

- Funding readiness

- Post-tax planning

- Financial visibility through CAS

While those topics may appear unrelated on the surface, they are all connected by the same underlying issue:

understanding how cash moves through a business operationally.

Cash flow is not a separate issue.

It is the operational foundation that everything else depends on.

Closing Thought

Most cash flow problems don’t come from a lack of income.

They come from a lack of structure.

Once you can clearly see:

- What’s coming in

- What’s going out

- And when it’s happening

You can start making decisions with confidence instead of reacting under pressure.

Predictability creates confidence.

That’s when a business begins to feel stable—not just successful.

Want a Clearer Picture of Your Cash Flow?

If your business is profitable but cash still feels unpredictable, the issue may not be revenue—it may be visibility.

We’ve created a Cash Flow Visibility Worksheet to help business owners identify timing gaps, recurring pressure points, and upcoming obligations before they create stress.

And if you need help building a more intentional reporting and forecasting structure, our team can help you create systems that support proactive decision-making—not just year-end reporting.

This article is provided for general informational purposes and does not constitute legal or tax advice.

2026 Meal Deduction Changes: What Businesses Need to Know

Most business owners don’t think about meal deductions until tax time—but the 2026 meal deduction changes could create unexpected impacts.

Recent tax law changes are quietly eliminating or limiting many common employer meal deductions, shifting how businesses should think about everyday expenses like team lunches, snacks, and on-site food.

Executive Summary

Starting in 2026, many employer-provided meals that were previously deductible will no longer be allowed as a tax deduction. While some business meals remain partially deductible, others—especially convenience meals and in-office food—become fully nondeductible. The real opportunity is no longer the deduction itself—it’s how expenses are planned, tracked, and structured throughout the year.

Not sure how your meal expenses will be treated in 2026?

Start with a simple decision guide and documentation checklist.

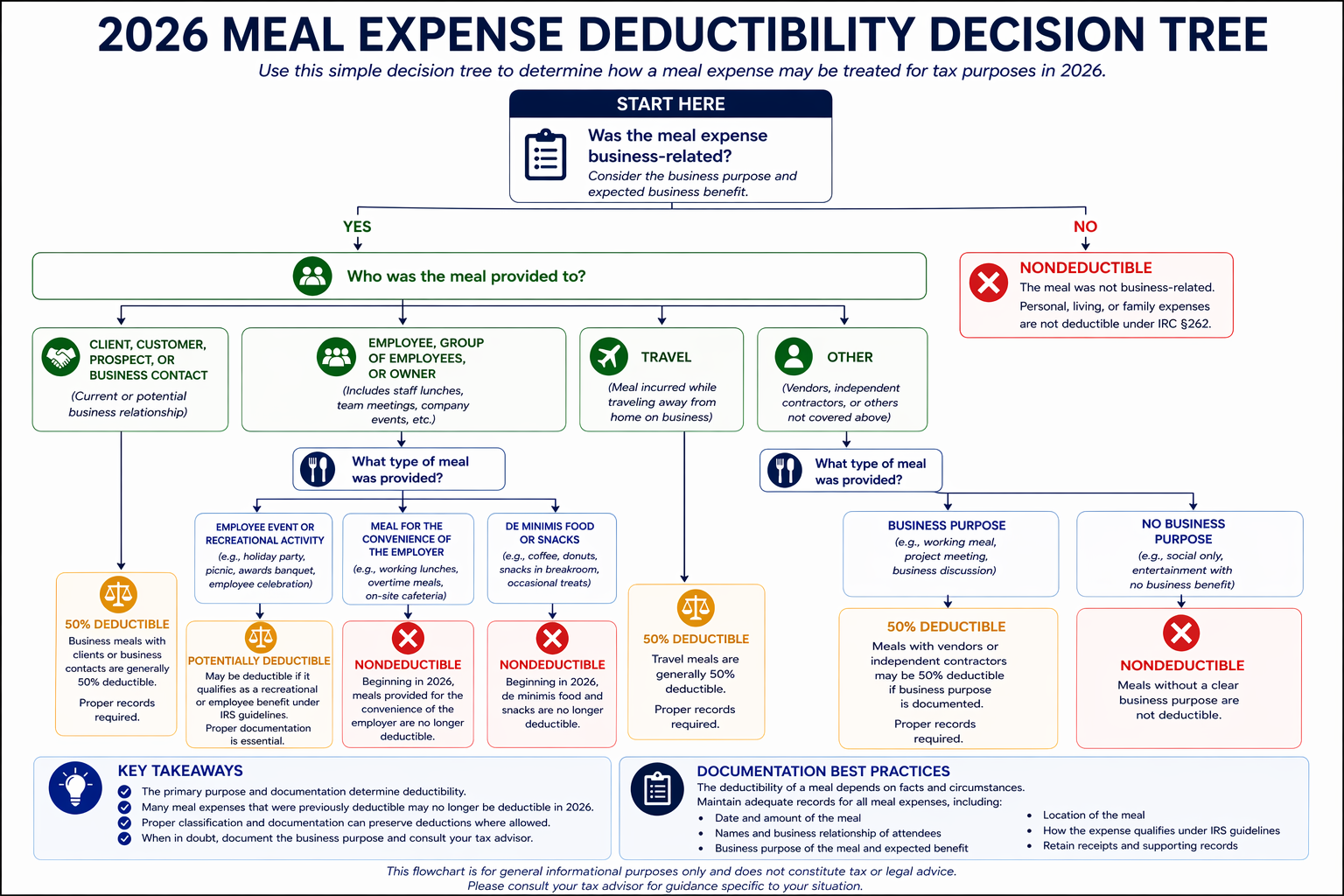

What Changed in Meal Deductions in 2026

Beginning January 1, 2026, several long-standing meal deductions have been eliminated under federal tax law.

Meals that are now nondeductible:

- Meals provided for the convenience of the employer

- On-site cafeterias and breakroom food

- De minimis snacks (coffee, snacks, occasional food)

Meals that are remain partially deductible:

- Business meals with clients or prospects (generally 50%)

Many everyday workplace food expenses are shifting from “routine deduction” to “fully taxable cost.”

Key Insight:

This isn’t just a tax change—it’s a visibility issue inside your financials. Most businesses don’t track meal expenses at a level detailed enough to apply these rules correctly.

See How Your Expenses Would Be ClassifiedCommon Real-World Scenarios

- Staff appreciation lunches — Generally nondeductible beginning in 2026

- Food ordered for internal meetings — Typically nondeductible

- Breakroom snacks and coffee — Nondeductible

- Client lunches — Still 50% deductible if properly documented

How Would Your Expenses Be Treated?

Not all meal expenses are treated the same. The outcome depends on purpose, structure, and documentation.

These 2026 meal deduction rules are best understood through a simple decision framework.

Use this decision guide to see how your expenses may be classified under the 2026 rules:

Want a printable version of this decision tree and a tracking checklist? Download the full guide below.

Where Strategy Still Creates Opportunity

At first glance, the 2026 changes feel like a simple loss of deductions. But in practice, the outcome depends heavily on how expenses are structured and documented. The same type of expense can be treated very differently for tax purposes depending on intent, documentation, and how it is categorized.

That means the outcome is no longer determined at tax time—it’s determined at the point the expense is recorded.

Example: Staff Appreciation Lunches

A typical team lunch may now be considered nondeductible if it is treated as a routine internal expense. However, in certain cases, similar expenses may still qualify for more favorable treatment when properly structured.

- Meals tied to company-wide events or structured employee activities may qualify differently

- Events that meet specific criteria (such as recreational or employee benefit classifications) may retain deductibility

- Proper documentation of purpose, attendees, and business intent becomes critical

What changes the outcome?

It’s not just the expense itself—it’s how it is framed and supported:

- Clear classification in the accounting system

- Consistent documentation of business purpose

- Separation between routine meals and structured events

- Alignment with IRS-defined categories

In other words, two businesses could spend the same amount on employee meals—and end up with very different tax outcomes.

The deduction isn’t gone—it’s conditional.

When expenses are planned and documented intentionally, opportunities still exist. When they’re not, deductions are simply lost.

This is where proactive planning—and structured financial systems like Client Accounting Services (CAS)—make the difference.

Download the Meal Deduction Guide

Compliance vs. Strategy

It’s easy to treat this as a compliance issue. But the more important question is how your business should adjust.

- Are meal expenses being categorized correctly in real time?

- Are deductible and nondeductible meals being clearly separated?

- Is management aware of the true after-tax cost of these expenses?

Advisory Perspective:

Most businesses don’t have a deduction problem—they have a tracking problem. Small classification issues can compound into larger reporting gaps.

How to Prepare for 2026

- Review and update expense categories in your accounting system

- Train staff on how to code meal-related expenses

- Separate internal meals from client-related meals

- Build reporting that reflects true after-tax costs

Closing Thought

The 2026 meal deduction changes are not dramatic on their own. But they are part of a broader shift from reactive tax compliance to proactive financial management. If you’re reviewing your financial systems after tax season, start with our post-tax reset checklist.

Not sure if your current setup supports these rules?

We’ll walk through your current process, identify gaps, and help you determine how to maximize your meal deductions.

Schedule a Meal Expense Review

This article is provided for general informational purposes and does not constitute legal or tax advice.

What Are Client Accounting Services (CAS)—and When Do They Make Sense for Your Business?

If you’re evaluating how to manage your business’s accounting and financial processes, this overview will help you understand your options—and when additional support makes sense.

Executive Summary

Client Accounting Services (CAS) go beyond traditional bookkeeping. They provide businesses with ongoing financial insight, structure, and decision support—without the cost of building an internal accounting department.

For growing businesses, CAS often fills the gap between “doing it yourself” and hiring a full in-house team.

What Are Client Accounting Services (CAS)?

Client Accounting Services (CAS) are best understood not as a single service, but as an ongoing financial support model.

Rather than hiring and managing an internal accounting team, businesses rely on CAS to bring together day-to-day financial operations, reporting, and advisory support in a coordinated way.

This approach allows business owners to move beyond simply recording transactions and instead focus on understanding performance, managing cash flow, and making more informed decisions as the business grows.

What CAS Typically Includes

CAS is not a single service—it’s a coordinated system of financial operations, reporting, and advisory support designed to give business owners clarity and confidence.

Core Financial Operations

- Bookkeeping and transaction management

- Accounts payable (vendor bill management and payments)

- Accounts receivable (invoicing and collections support)

- Payroll coordination and processing (especially with evolving reporting requirements)

- Bank and credit card reconciliations

- General ledger maintenance and journal entries

Financial Reporting & Visibility

- Monthly financial statements

- Cash flow tracking

- General Ledger Account reconciliations

- Customized reporting

- Financial dashboards and visibility tools

Compliance & Regulatory Support

- Payroll tax return preparation and filing

- W-2 and 1099 preparation

- Sales, use, property, and B&O tax compliance

Planning & Advisory Support

- Budgeting and forecasting

- Cash flow planning (and how it ties into growth and funding decisions)

- KPI tracking and performance insights

- Ongoing financial guidance

- Financial process improvement

In addition to ongoing CAS support, many businesses benefit from coordinated services such as entity structuring, tax planning, and estate or succession considerations—all of which should align with your broader financial strategy.

Why This Matters

Most businesses don’t struggle because they lack data—they struggle because they lack clear, timely, and actionable financial insight to guide decisions.

This becomes especially important when financial planning, funding, or compliance requirements increase.

CAS bridges that gap by combining day-to-day financial management with forward-looking guidance.

CAS is not one-size-fits-all. It’s typically structured around what you need today—with the ability to grow as your business evolves.

The Problem Many Businesses Face

As businesses grow, financial complexity increases—but internal processes often don’t keep up.

Common challenges we see:

- Financials are behind or unclear

- Owners are making decisions without reliable data

- Bookkeeping is handled inconsistently or reactively

- No clear view of cash flow or upcoming obligations

- Time is spent managing admin instead of running the business

At a certain point, the question becomes:

Do we build this internally—or look for outside support?

Are your financials helping you make decisions—or just recording history?

If you’re spending time managing bookkeeping, questioning your numbers, or making decisions without clear financial insight, you’re not alone. Many growing businesses reach a point where their current process can’t keep up.

Option 1: Keeping Accounting In-House

What it looks like: Hiring a bookkeeper or building an internal team

Pros:

- Direct control over processes

- Immediate access to information

- Familiarity with internal operations

Challenges:

- Cost of salaries, benefits, and training

- Limited expertise (typically one skill set per hire)

- Risk of gaps if someone leaves

- Difficult to scale as the business grows

For many small to mid-sized businesses, building a full accounting function internally is more expensive—and less robust—than expected.

Option 2: Large Outsourced Accounting Providers

What it looks like: National firms or platform-based accounting services

Pros: